Nau Mai, Haere mai

Through this website, the Trust will provide updates on news, events, and information on the activities of the Trust for members, whanau, and the general public.

He Tohu Whakamaarama.

Our logo represents the unique and iconic “reti board” that is synonymous with Ngāti Pāhauwera. The “reti board” is a Ngāti Pāhauwera exemplar of an ancient creation of innovation in catching the world-famous Mohaka kahawai. Symbolised within the body of the “reti board” is “Paikea”, revered taniwha of the Mohaka. The Mohaka, Waihua and Waikare rivers are reflected in the logo background.

Ngāti Pāhauwera Development Trust

E mihi ana ki te iti me te rahi o Ngāti Pāhauwera. Kō nei tonu te ipurangi whakairi kōrero hei tirotiro mā ngā urī o Ngāti Pāhauwera. Me mihi atu hoki ki te hunga i tua atu i te Iwi e pānui ana i ngā kōrero mō mātau, tēnā anō koutou katoa..

PAHAUWERA PROFILES

Our Register

Register and update your details

NEW REGISTRATIONS

The Trust also invites anyone who has not already enrolled, aged 18 years and over and with the appropriate whakapapa, to apply to be included on the Trust’s register. Registration forms are available from the Trust offices, 74 Queen Street, Wairoa or 170a Waghorne Street, Napier. It will allow us to identify who and where who and where our whānau are, thereby helping the Trust to better serve our whānau and Hapū.

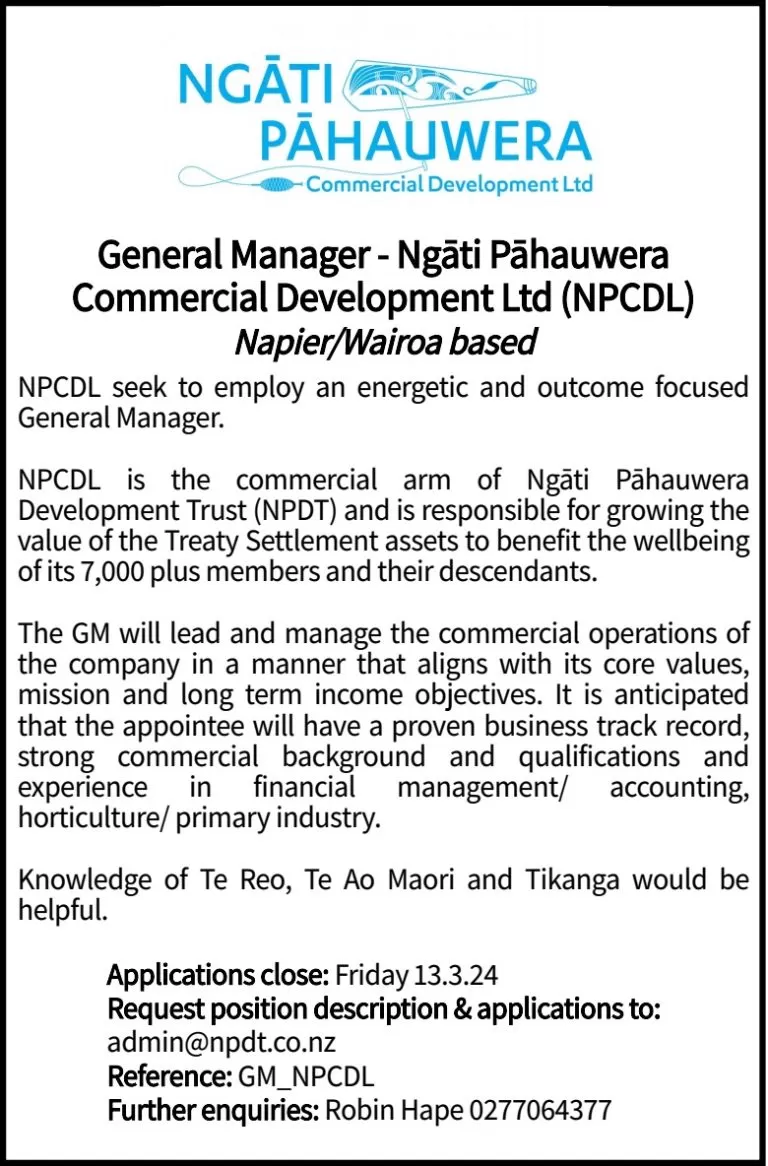

Employment Opportunity

Te Oranganui o Ngāti Pāhauwera

A supportive, healthy, vibrant, prosperous and united Ngāti Pāhauwera.

Te Paerangi Kei Mua – Mission

To protect and enhance the resources of Ngāti Pāhauwera for the welfare of the people and to maintain the Treaty claim settlement in a sustainable manner for future generations.

Nga Tikanga – Guiding Principles

- Ko te Amorangi ki mua ko te hapai o ki muri.

Let Io be the spearhead and achievement will follow.

- Mahia nga māhi o Kahukura

Imagine and create a better future.

- Kia ū ki te pā harakeke

Cherish your whanau, hapu, iwi.

- Ko taku rekereke ko taku tūrangawaewae

Wherever I live, I stand as Ngāti Pāhauwera.

- Pakatō i te ata, Pakatō i te ahiahi, Maurī mahi Mauri ora.

Planning and preparation are critical to health and prosperity.

- Mōhaka harara taupunga ōpunga.

United in our diversity.

- Ko au te awa, ko te awa ko au.

I am the river and the river is me. The river is integral to my identity.